Impact Accounting and Hourly Matching: A Review of the Research into Outcomes

Download the metastudy paper PDF: Impact Accounting and Hourly Matching: A Review

The GHG Protocol is currently considering two different proposals for how emissions from electricity (Scope 2) are reported, which could have significant repercussions on the future of renewable energy purchasing. The two separate proposals are a) local hourly matching, which counts renewable energy only in the same location and hour it is consumed, and b) consequential impact accounting, which counts the total impact on emissions of an action. With corporations purchasing over 270 TWh of renewable energy in 2024, understanding the way that these reporting standards could shape those purchasing decisions is critical for the future of grid decarbonization.

Over the past year, a notable pattern has emerged in discussions convened through the ZEROgrid Impact Advisory Initiative between proponents of hourly matching and those favoring consequential approaches to clean energy procurement. Across these conversations, there was consensus on how to estimate the impact of renewable procurement: the change in total long-run real-world emissions compared with the scenario in which the procurement did not take place, recognizing that this hypothetical counterfactual scenario can often only be estimated but not directly measured. Disagreements were not on the definition of impact, but on how to best achieve impact and whether that emissions reduction impact should be the primary criterion to set an accounting standard around.

The ZEROgrid Impact Advisory Initiative discussions led to two concrete outcomes. The first was the ZEROgrid white paper, jointly authored by both hourly matching and consequential advocates, clarifying the above definition of success. The second was recognition of a need for what we called the “impact metastudy”, to examine all available research on a single question: what is the effect on this impact of different accounting standards and the procurement methods they promote?

This idea found widespread support in several circles. At the June 2024 NREL/RMI workshop, a group of 30 companies and emissions experts endorsed the need for an impact metastudy. Work from numerous experts, in ZEROgrid and not, is used in the impact metastudy. In September 2025, Climate Breakthrough Foundation selected these kinds of impact metastudies for carbon accounting as one of the five most promising climate breakthroughs of 2025.

Over the past year, WattTime has conducted work on the aforementioned impact metastudy. This metastudy comprises various studies on the impact of different possible carbon accounting standards. “Impact” is defined consistently with the first ZEROgrid report: reductions in total, real-world, long-run emissions, which are precisely mathematically defined, whether or not we are able to directly measure them.

To do this, we considered existing studies and worked to fill in gaps with new studies. The existing and new studies include:

- A study summarizing the existing published literature, including publications by Xu et al., Riepin and Brown, and E3.

- A study using long-run emissions rates from NREL’s Cambium model to compare the costs and impacts of hourly matching and impact accounting in the US.

- A study comparing the impact of renewables in locations worldwide using UNFCCC marginal emissions rates.

- A study that compared cost and impacts of both proposed standards worldwide using long-run emissions rates from Climate TRACE. These are important because much of the prior analysis was limited to the US and Europe.

- A study in collaboration with Open Energy Transition, using the PyPSA capacity expansion and dispatch model to analyze the impact of different ways of implementing the hourly matching standard, found that the way the current proposal is written could significantly reduce the impact from what was previously studied.

A further study, using data from Transition Zero, is also currently under development, so that chapter of this review is still forthcoming.

We used a variety of methods and models to perform these analyses to get a fuller picture of the outcomes of implementing these proposed standards, in order to understand what outcomes these different models agreed on. Today, we are publishing a review summarizing both our research and other relevant publications from other researchers [1,2,3]. Across the studies, we find four robust conclusions:

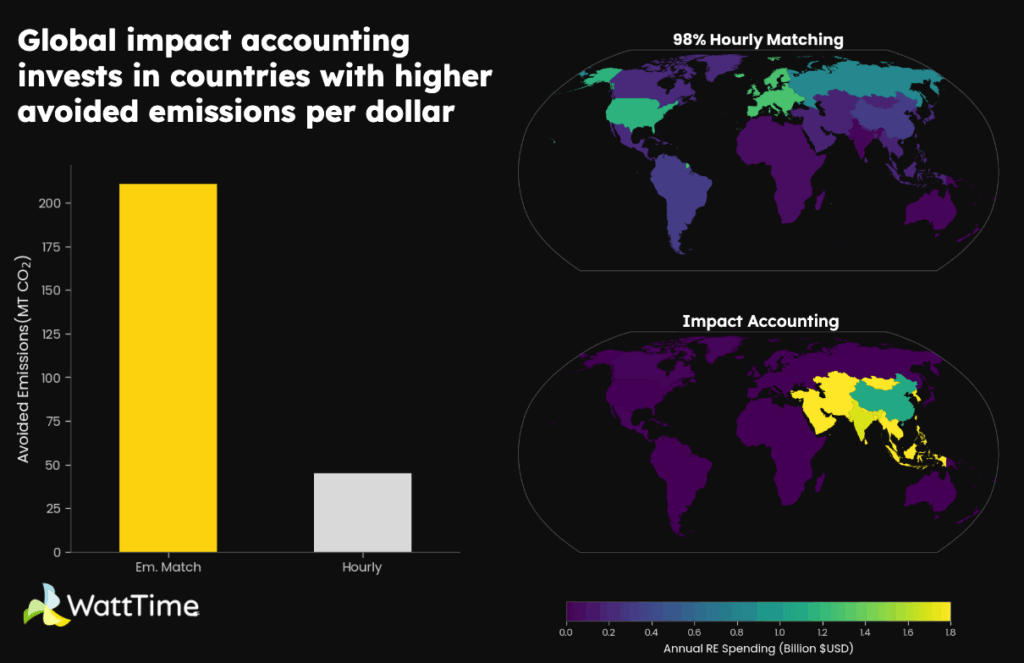

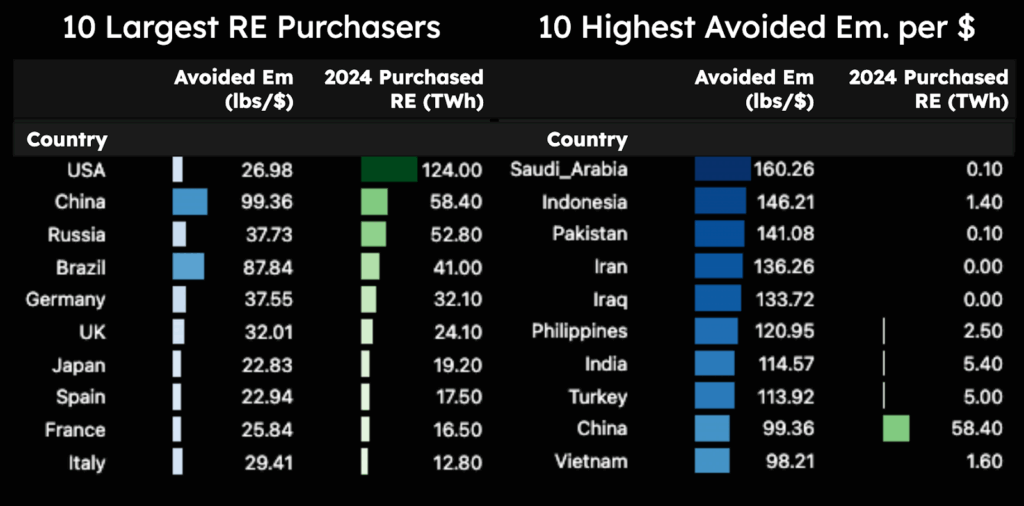

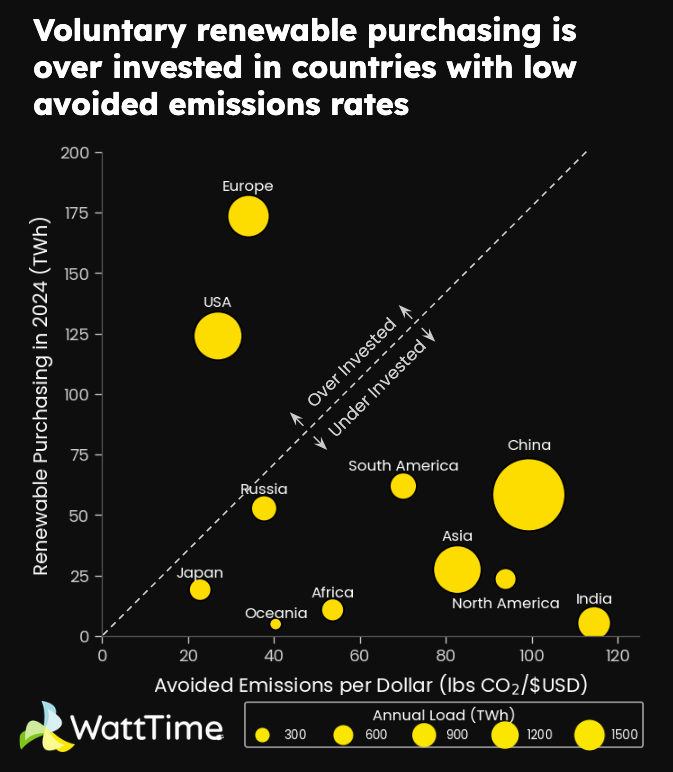

- Location matters more than timing. The location of renewable procurement has a much larger effect on emissions outcomes than timing. Investing in high-emitting grids consistently yields substantially greater avoided emissions per dollar than investments that restrict procurement to the consumer’s local grid. Timing also has an important impact on emissions, but generally less than location. Where matching generation by location and hour only counts clean energy locally to a company's own facilities, optimization of generation resources prioritizes renewables in the times and places where emissions impact is greatest.

- Impactful hourly matching portfolios come at a high cost. In some cases, high degrees of hourly matching with local matching/deliverability and additionality requirements can reduce more emissions than consequential-based procurements. This result is primarily from a “volume effect”, whereby companies must purchase far more renewable energy than they consume to achieve a high hourly matching rate. However, the need to purchase these excess volumes, coupled with restrictions on where and when the energy can be purchased, imposes steep cost premiums. Crucially, these costs are likely to reduce the willingness of companies to participate in voluntary procurement. As a result, the total emissions impact can be expected to be substantially lower than prior research, which did not account for this behavioural response, had assumed.

- Consequential Impact Accounting can address global inequity in renewables. An emissions matching strategy using impact accounting directs capital toward emerging economies that have long been underserved by renewable investment, delivering greater emissions reductions while advancing global equity and providing benefits such as improved air quality, lower electricity costs, and expanded access to clean energy jobs in these regions.

- An additionality requirement is essential for impact. Meaningful emissions reductions depend on strong additionality requirements: without strict rules that prevent counting pre-existing clean energy assets, even very high levels of hourly matching yield little real emissions benefit.

These conclusions have strong implications for how a revision to the accounting standards will impact total global emissions. The currently proposed local hourly matching standard is likely to come at a high cost that could reduce total participation in voluntary procurement. Without a stronger additionality constraint, procurement will not lead to actual reductions in emissions. And a local deliverability requirement may reinforce the existing bias towards investing in relatively clean grids in the USA and Europe. By contrast, a consequential impact accounting standard could guide renewable energy purchasing into the dirtiest grids where projects have the most cost-effective impact on reducing emissions. This freedom in location could also lead to an expansion of investment in the Global South, where grids are dirtiest and renewable investment is the lowest today. A consequential reporting standard focused on emissions could provide the strongest signals to voluntary corporate renewable energy purchasers to reduce more global greenhouse gas emissions more quickly.

WattTime would like to especially thank Climate Breakthrough for the majority funding of this research. Thank you also to Apple, Meta Platforms, HPE Foundation, James and Kaye Slavet, and Reid Hoffman for providing funding or support. Thanks to Gurobi for providing access to their linear optimization software. The views expressed in the article do not necessarily represent the views of the sponsors.

Download the metastudy paper PDF: Impact Accounting and Hourly Matching: A Review

If you’re concerned about how the proposed revisions to Scope 2 could negatively impact your business or would just like to share your perspective with the GHG Protocol, they are accepting comments here through January 31, 2026. If you’d like more help navigating the two separate proposals and the two lengthy surveys, we’ve provided more guidance here.